Polynomial and Flexible Regression#

Let us have a quick recap of the first session of the semester, where regression models were introduced. In linear regression, we assume that the relationship between a predictor \(x\) and a response \(y\) is a straight line:

In many real-world problems, this assumption is too restrictive. The true relationship may be curved, bend differently in different regions of \(x\), or vary smoothly but non-linearly.

In this chapter, we look at four families of methods that allow more flexible regression functions:

Polynomial regression

Stepwise regression

Spline regression

Local regression

Let’s start by creating some example data. Imagine we have one predictor \(x\) and a response \(y\) generated as:

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

rng = np.random.default_rng(42)

n = 200

X = np.linspace(0, 10, n)

eps = rng.normal(scale=0.4, size=n)

y = np.sin(X) + 0.3 * X + eps

data = pd.DataFrame({"x": X, "y": y})

fig, ax = plt.subplots()

ax.scatter(data["x"], data["y"], alpha=0.5)

ax.set(xlabel="x", ylabel="y");

If we fit a straight line to such data, the model will clearly miss the oscillating pattern. Flexible regression methods aim to recover such non-linear patterns while still being based on the same least squares framework.

Polynomial Regression#

Polynomial regression extends the linear model by including powers of \(x\) as additional predictors:

Degree 1 (ordinary linear regression):

\[ y \approx \beta_0 + \beta_1 x \]Degree 2 (quadratic):

\[ y \approx \beta_0 + \beta_1 x + \beta_2 x^2 \]Degree \(d\):

\[ y \approx \beta_0 + \beta_1 x + \beta_2 x^2 + \dots + \beta_d x^d. \]

Note

Polynomial regression models are still linear models in the parameters \((\beta_0, \dots, \beta_d)\) – we just feed them transformed inputs \((x, x^2, \dots, x^d)\).

Pros:

Simple and easy to fit with ordinary least squares

Can capture smooth non-linear trends with low-degree polynomials

Cons:

High-degree polynomials can oscillate wildly (especially at the boundaries)

Global basis: changing the fit in one region can affect the entire curve

We can conveniently generate polynomial features using PolynomialFeatures from sklearn.preprocessing and then fit a standard LinearRegression model.

from sklearn.preprocessing import PolynomialFeatures

from sklearn.linear_model import LinearRegression

def fit_poly_regression(x, y, degree):

"""Fit a polynomial regression of given degree and return the model + grid predictions."""

x = np.asarray(x).reshape(-1, 1)

poly = PolynomialFeatures(degree=degree, include_bias=False)

X_poly = poly.fit_transform(x)

model = LinearRegression()

model.fit(X_poly, y)

# For visualisation: predictions on a dense grid

x_grid = np.linspace(x.min(), x.max(), 300).reshape(-1, 1)

X_grid_poly = poly.transform(x_grid)

y_hat = model.predict(X_grid_poly)

return model, x_grid.ravel(), y_hat

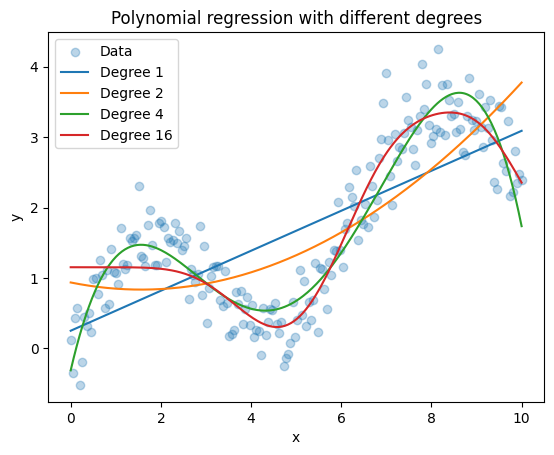

degrees = [1, 2, 4, 16]

fig, ax = plt.subplots()

ax.scatter(data["x"], data["y"], alpha=0.3, label="Data")

for d in degrees:

_, xg, yg = fit_poly_regression(data["x"], data["y"], degree=d)

ax.plot(xg, yg, label=f"Degree {d}")

ax.set(xlabel="x", ylabel="y", title="Polynomial regression with different degrees")

plt.legend();

Things to observe:

Degree 1 (straight line) cannot follow the curvature.

Degree 2 or 3 often works well for gently curved relationships.

Higher degree models can start to wiggle and overfit the noise.

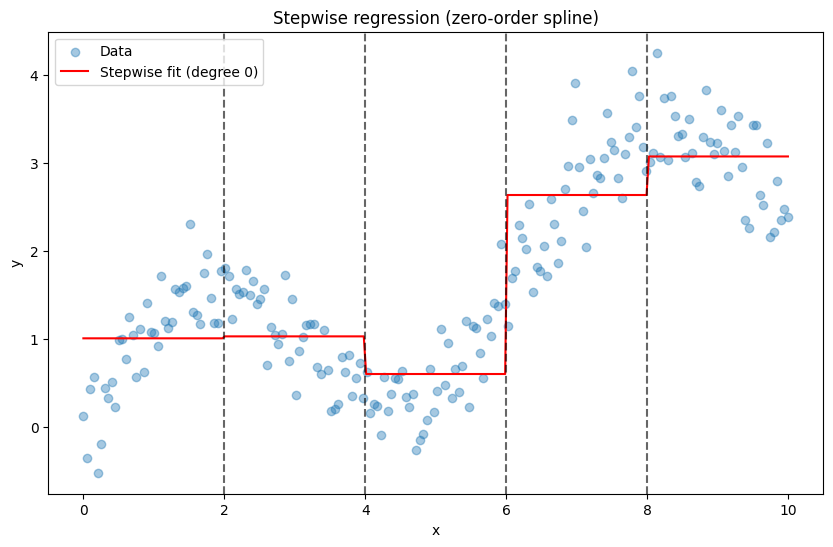

Piecewise Constant Regression#

The simple idea:

Divide the range of \(x\) into intervals using cut points (knots) and fit a constant mean within each interval.

Concretely, choose cut points \(c_1 < c_2 < \dots < c_K\) and define indicator variables

Then the model is

which produces a piecewise constant (stepwise) regression function. This is equivalent to a B-spline of degree 0 (a “zero-order spline”).

Pros:

Very simple and interpretable: one mean per age/

x-intervalUseful as a starting point to understand more flexible splines

Cons:

The fit is discontinuous at the cut points

Sensitive to the choice and placement of cut points

Can look rough; higher-order splines often give smoother fits

We can build a 0th-order spline (step function) basis using patsy.dmatrix with bs(..., degree=0) and then fit a linear model with statsmodels:

import patsy

import statsmodels.api as sm

# Choose some cut points (knots) over the x-range

cut_points = (2, 4, 6, 8)

# Build a B-spline basis of degree 0 (step function)

transformed_x = patsy.dmatrix(

"bs(x, knots=cut_points, degree=0, include_intercept=False)",

{"x": data["x"], "cut_points": cut_points},

return_type="dataframe",

)

Fit the model:

step_model = sm.OLS(data["y"], transformed_x)

step_fit = step_model.fit()

print(step_fit.summary())

OLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.757

Model: OLS Adj. R-squared: 0.752

Method: Least Squares F-statistic: 152.2

Date: Wed, 04 Mar 2026 Prob (F-statistic): 8.05e-59

Time: 12:27:54 Log-Likelihood: -167.85

No. Observations: 200 AIC: 345.7

Df Residuals: 195 BIC: 362.2

Df Model: 4

Covariance Type: nonrobust

=================================================================================================================================

coef std err t P>|t| [0.025 0.975]

---------------------------------------------------------------------------------------------------------------------------------

Intercept 1.0069 0.090 11.227 0.000 0.830 1.184

bs(x, knots=cut_points, degree=0, include_intercept=False)[0] 0.0223 0.127 0.176 0.861 -0.228 0.272

bs(x, knots=cut_points, degree=0, include_intercept=False)[1] -0.4055 0.127 -3.197 0.002 -0.656 -0.155

bs(x, knots=cut_points, degree=0, include_intercept=False)[2] 1.6288 0.127 12.843 0.000 1.379 1.879

bs(x, knots=cut_points, degree=0, include_intercept=False)[3] 2.0670 0.127 16.297 0.000 1.817 2.317

==============================================================================

Omnibus: 0.227 Durbin-Watson: 0.792

Prob(Omnibus): 0.893 Jarque-Bera (JB): 0.357

Skew: -0.062 Prob(JB): 0.837

Kurtosis: 2.834 Cond. No. 5.83

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

Visualise the stepwise fit:

xp = np.linspace(data["x"].min(), data["x"].max(), 300)

xp_trans = patsy.dmatrix(

"bs(xp, knots=cut_points, degree=0, include_intercept=False)",

{"xp": xp, "cut_points": cut_points},

return_type="dataframe",

)

pred_step = step_fit.predict(xp_trans)

plt.figure(figsize=(10, 6))

plt.scatter(data["x"], data["y"], alpha=0.4, label="Data")

plt.plot(xp, pred_step, color="red", label="Stepwise fit (degree 0)")

for c in cut_points:

plt.axvline(c, color="black", linestyle="--", alpha=0.6)

plt.xlabel("x")

plt.ylabel("y")

plt.title("Stepwise regression (zero-order spline)")

plt.legend();

Spline Regression#

The previous section introduced “stepwise regression” as 0th-order splines. However, when we talk about spline regression, we usually mean higher-order splines, which will smooth these steps into continuous and differentiable curves. Again, the key idea is the similar:

Approximate the regression function by piecewise polynomials that are smoothly joined at pre-defined points called knots.

For example, a cubic spline with knots at \(t_1, \dots, t_K\) is a function that is:

A cubic polynomial on each interval \((-\infty, t_1)\), \((t_1, t_2)\), …, \((t_K, \infty)\)

Continuously differentiable up to a certain order at the knots

We usually do not work with the piecewise form directly. Instead, we represent splines as a linear combination of basis functions:

where \(B_j(x)\) are spline basis functions (B-splines). This again gives a linear model in the parameters \(\theta_j\).

Two common options:

B-splines (flexible general basis)

Natural splines (add boundary constraints to avoid wild extrapolation)

Again, we use the convenient bs() function from patsy to create B-spline bases. We can then plug these into statsmodels for ordinary least squares:

from patsy import dmatrix

# Build a cubic B-spline basis with 6 degrees of freedom

spline_basis = dmatrix(

"bs(x, df=6, degree=3, include_intercept=False)",

{"x": data["x"]},

return_type="dataframe",

)

Fit an OLS model:

spline_model = sm.OLS(data["y"], spline_basis).fit()

print(spline_model.summary())

OLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.906

Model: OLS Adj. R-squared: 0.903

Method: Least Squares F-statistic: 308.2

Date: Wed, 04 Mar 2026 Prob (F-statistic): 5.30e-96

Time: 12:27:54 Log-Likelihood: -73.555

No. Observations: 200 AIC: 161.1

Df Residuals: 193 BIC: 184.2

Df Model: 6

Covariance Type: nonrobust

=====================================================================================================================

coef std err t P>|t| [0.025 0.975]

---------------------------------------------------------------------------------------------------------------------

Intercept -0.2490 0.155 -1.604 0.110 -0.555 0.057

bs(x, df=6, degree=3, include_intercept=False)[0] 1.8920 0.290 6.527 0.000 1.320 2.464

bs(x, df=6, degree=3, include_intercept=False)[1] 2.0838 0.189 11.049 0.000 1.712 2.456

bs(x, df=6, degree=3, include_intercept=False)[2] -0.6812 0.231 -2.947 0.004 -1.137 -0.225

bs(x, df=6, degree=3, include_intercept=False)[3] 4.6825 0.214 21.838 0.000 4.260 5.105

bs(x, df=6, degree=3, include_intercept=False)[4] 3.3392 0.241 13.834 0.000 2.863 3.815

bs(x, df=6, degree=3, include_intercept=False)[5] 2.7045 0.216 12.516 0.000 2.278 3.131

==============================================================================

Omnibus: 2.725 Durbin-Watson: 1.790

Prob(Omnibus): 0.256 Jarque-Bera (JB): 2.671

Skew: 0.281 Prob(JB): 0.263

Kurtosis: 2.933 Cond. No. 19.7

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

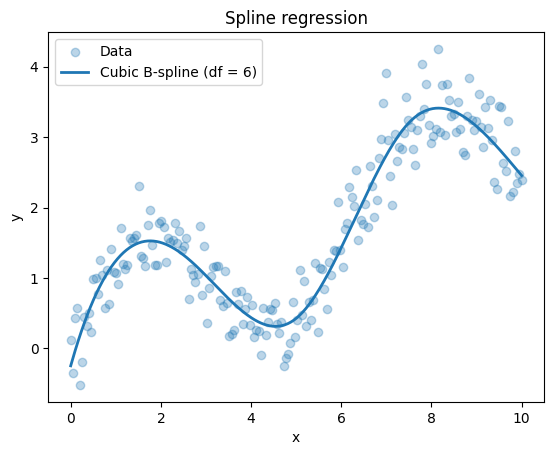

Visualise the spline fit:

x_grid = np.linspace(data["x"].min(), data["x"].max(), 300)

spline_grid = dmatrix(

"bs(x, df=6, degree=3, include_intercept=False)",

{"x": x_grid},

return_type="dataframe",

)

y_spline_hat = spline_model.predict(spline_grid)

fig, ax = plt.subplots()

ax.scatter(data["x"], data["y"], alpha=0.3, label="Data")

ax.plot(x_grid, y_spline_hat, label="Cubic B-spline (df = 6)", linewidth=2)

ax.set_xlabel("x")

ax.set_ylabel("y")

ax.set_title("Spline regression")

ax.legend();

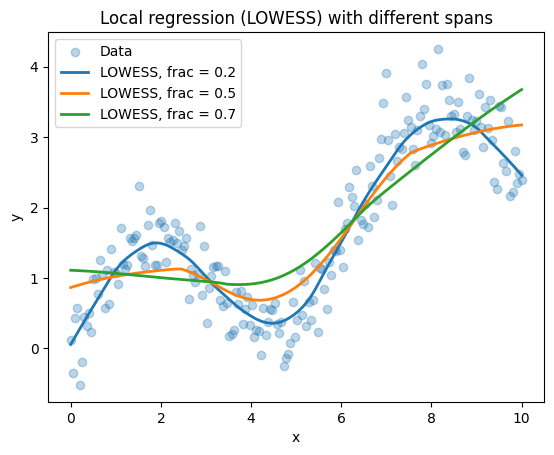

Local Regression (LOWESS)#

Polynomial and spline regression still use a global basis: one set of parameters applies to the whole range of \(x\). Local regression takes a different view:

Fit a separate regression in a neighbourhood around each target point, using only nearby observations (with weights).

For a target point \(x_0\):

Define a neighbourhood around \(x_0\), e.g. the closest \(\alpha \cdot n\) observations, where \(\alpha\) is a smoothing parameter between 0 and 1.

Assign weights to observations, typically higher for points closer to \(x_0\).

Fit a weighted least squares regression (often linear or quadratic) using those weighted points.

The fitted value at \(x_0\) is the prediction from this local model.

Repeat this for many \(x_0\) to obtain a smooth curve.

Key parameters:

Span / fraction (

frac): proportion of data used in each local fitSmall

frac→ very flexible, risk of overfittingLarge

frac→ smoother, less flexible

Degree of local polynomial (often 1 or 2)

statsmodels provides a convenient implementation of LOWESS (locally weighted scatterplot smoothing).

from statsmodels.nonparametric.smoothers_lowess import lowess

x = data["x"].to_numpy()

y = data["y"].to_numpy()

# Try different fractions

frac_list = [0.2, 0.5, 0.7]

fig, ax = plt.subplots()

ax.scatter(x, y, alpha=0.3, label="Data")

for frac in frac_list:

result = lowess(y, x, frac=frac, return_sorted=True)

ax.plot(result[:, 0], result[:, 1], label=f"LOWESS, frac = {frac}", linewidth=2)

ax.set(xlabel="x", ylabel="y", title="Local regression (LOWESS) with different spans")

ax.legend();

Observe:

frac = 0.2follows the data more closely (more wiggles).frac > 0.5give a more general trend.

Local regression methods are very useful for exploratory analysis: they give a flexible, data-driven summary of the trend without a strong global parametric assumption.

Summary and Quiz#

Method |

Key Idea |

Flexibility |

Pros |

Cons |

|---|---|---|---|---|

Polynomial Regression |

Powers of \(x\) as predictors: \(x, x^2, \dots, x^d\) |

Controlled by degree \(d\) |

Simple to fit with OLS; interpretable |

Oscillates at boundaries; global changes affect entire curve |

Piecewise Constant Regression |

Constant values in intervals defined by knots |

Controlled by knots |

Simple and interpretable |

Discontinuous at knots; sensitive to knot placement |

Spline Regression |

Piecewise polynomials smoothly joined at knots |

Controlled by knots and degree |

Smooth and flexible; mostly local |

Requires choosing knots; can overfit with many knots |

Local Regression (LOWESS) |

Weighted regression in neighborhood of each point |

Controlled by span/fraction |

Data-driven; no global assumptions |

Computationally intensive; requires choosing span; harder to interpret |

In the lecture, all methods except simple polynomial regression are considered local models. In piecewise constant regression, only the information within each bin contributes to the fitted value in that region. Spline regression is also largely local, but neighbouring intervals are coupled through smoothness constraints at the knots, which introduces a limited amount of global structure.

In practice, these methods are often combined with regularisation and cross-validation to control overfitting and to select tuning parameters such as the degree, number and location of knots, or the span.