6.2 Correlations#

Many Python packages, such as numpy, scipy, and pandas offer functionalities for correlation analysis. As we often work with data in the form of Pandas DataFrames, we will use the pandas package for now.

Pearson´s correlation

Pearson’s correlation coefficient is calculated as the ratio of the covariance of two variables X and Y to the product of their standard deviations:

Let’s start by creating a simple DataFrame containing an x and y variable:

import pandas as pd

data = {

'X': range(10, 20),

'Y': [2, 1, 4, 5, 8, 12, 18, 25, 96, 48]

}

df = pd.DataFrame(data)

print(df)

X Y

0 10 2

1 11 1

2 12 4

3 13 5

4 14 8

5 15 12

6 16 18

7 17 25

8 18 96

9 19 48

We can then calculate the correlation between these two variables by using the .corr() method. By default, this method calculates Pearson’s correlation coefficient:

correlation_coef = df['X'].corr(df['Y'])

print("Pearson's correlation:", correlation_coef)

Pearson's correlation: 0.7586402890911867

The .corr() method also allows you to use rank correlations (Spearman, Kendall) thrugh the method parameter. For example, you can calculate Spearman’s rank correlation as follows:

print("Spearman correlation:",

df['X'].corr(df['Y'],

method='spearman'))

Spearman correlation: 0.9757575757575757

Correlation Matrices#

If we want to compute correlations for multiple variables, handling individual correlations will not be feasible. In such cases, we can calculate and use correlation matrices, which contain all pairwise correlations. Let’s start by creating a new DataFrame with four variables and then compute the correlation matrix, rounding the results to two decimal places:

# Define the data

data = {

'A': [0, 1, 2, 3, 4, 5, 6, 7, 8, 9],

'B': [2, 1, 4, 5, 8, 12, 18, 25, 96, 48],

'C': [9, 7, 8, 6, 5, 4, 3, 2, 1, 0],

'D': [1, 3, 3, 5, 8, 3, 6, 12, 5, 34]

}

# Create a pandas DataFrame

df = pd.DataFrame(data)

# Compute the correlation matrix

corr_matrix = df.corr()

# Round the correlation matrix to 2 decimal places

corr_matrix_rounded = corr_matrix.round(2)

print(corr_matrix_rounded)

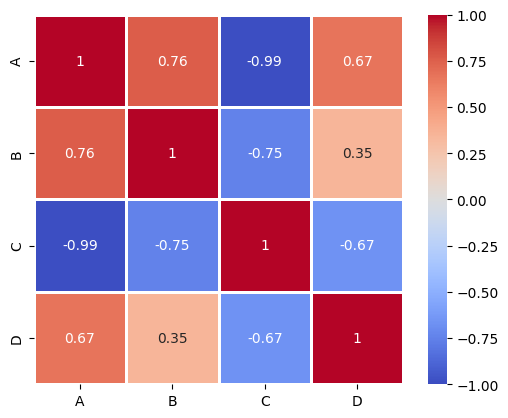

A B C D

A 1.00 0.76 -0.99 0.67

B 0.76 1.00 -0.75 0.35

C -0.99 -0.75 1.00 -0.67

D 0.67 0.35 -0.67 1.00

To make the results more visually appealing, we can plot the correlation matrix as a heatmap using the seaborn library:

import seaborn as sns

import matplotlib.pyplot as plt

sns.heatmap(corr_matrix_rounded,

annot=True, # Display correlation values inside the heatmap cells.

vmin=-1, vmax=1, # Define the limits of the color scale

square=True, # Make sure cells stay square

cmap="coolwarm", # Set the color map

linewidths=1 # Lines between the cells

)

plt.show()

Summary

You can calculate correlations with various packages. In Pandas, you can use the

.corr()method.A nice and intuitive way of visualizing multiple correlation values are correlation matrices (heatmaps).